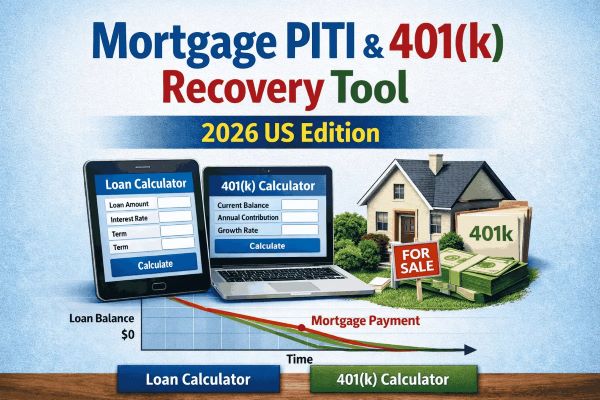

Mortgage PITI & 401(k) Recovery Tool: 2026 US Edition

Mortgage Profile

401(k) Growth Strategy

Financial Recovery Roadmap

Enter details to see your wealth strategy.

Mortgage PITI & 401(k) Recovery Tool: 2026 US Edition

Mortgage planning in the US is no longer just about EMIs—it’s about strategy. The Mortgage PITI & 401(k) Recovery Tool: 2026 US Edition is designed to help you understand how your home loan interacts with your retirement savings. It gives you a smarter way to compare home loan costs vs 401(k) investment growth, so you can make financially sound decisions.

Whether you’re planning to buy a house, already paying a mortgage, or thinking about early payoff—this tool helps you answer one key question:

👉 Should you invest more or pay off your loan faster?

Mortgage PITI & 401(k) Recovery Tool 2026 (US Edition)

This advanced calculator combines two major financial elements:

- PITI (Principal, Interest, Taxes, Insurance) → Total cost of your home loan

- 401(k) Growth Potential → Your long-term retirement investment returns

By using this tool, you can perform:

- Home Loan vs 401(k) Calculator

- Cost Comparison Home Loan Calculator with 401(k) Growth Comparison

- Retirement Strategy Mortgage Interest Recovery Tool

It helps you analyze whether investing in a 401(k) can offset your mortgage interest over time.

What is PITI in Mortgage?

PITI stands for:

- Principal – Loan amount you repay

- Interest – Cost of borrowing

- Taxes – Property taxes

- Insurance – Homeowner’s insurance

Your monthly mortgage payment includes all these components, making it essential to understand the true cost of your home loan.

Why Compare 401(k) Investment vs Home Loan Debt?

Many US homeowners face a common dilemma:

- Should I pay off my mortgage early?

- Or invest extra money into my 401(k)?

This tool helps you evaluate:

- Opportunity cost of paying off debt early

- Potential compounding growth in retirement savings

- Long-term wealth impact

👉 In many cases, 401(k) returns may outperform mortgage interest rates, especially with employer matching.

Key Features of This Tool

1. Home Loan Calculator with 401(k) Growth Comparison (US Edition)

Compare your loan repayment vs investment returns side-by-side. Check 401(k) historic returns on https://www.investopedia.com/.

2. Savings Optimizer – Pay Off Your Mortgage with 401(k) Gains

See how your investments can “cover” or exceed mortgage interest.

3. Home Loan Interest Offset Tool

Calculate how much of your loan interest can be neutralized through smart investing.

4. Retirement Strategy Mortgage Interest Recovery Tool

Build a strategy where your retirement savings compensate for mortgage costs.

5. Free Home Loan Strategy in US

Get actionable insights to reduce financial burden without guesswork.

How This Tool Works

Step 1: Enter Mortgage Details

- Loan amount

- Interest rate

- Loan term

- Property taxes & insurance

Step 2: Add 401(k) Inputs

- Contribution amount

- Employer match (if any)

- Expected return rate

Step 3: Analyze Results

The tool will show:

- Total mortgage cost (PITI-based)

- Total 401(k) future value

- Net gain/loss comparison

- Mortgage interest recovery potential

Home Loan vs 401(k) Calculator – Real Insight

This comparison gives you clarity on:

- Whether to prepay your mortgage

- Or invest aggressively in 401(k)

For example:

If your mortgage interest is 6% but your 401(k) returns 8–10%, investing may be the better option.

Recover Your Mortgage Interest with Investing

One of the biggest advantages of this tool is Mortgage Interest Recovery Analysis.

Instead of viewing mortgage interest as a loss, you can:

- Offset it through higher investment returns

- Build long-term wealth

- Maintain liquidity instead of locking funds in home equity

This is especially useful in the US, where:

- Mortgage interest rates fluctuate

- Retirement planning is self-driven

- 401(k) offers tax advantages

How To Get Free Home Loan in USA (Smart Strategy)

While a “free home loan” isn’t literal, you can neutralize its cost by:

- Investing consistently in 401(k)

- Taking advantage of employer match

- Avoiding unnecessary prepayments

- Refinancing at lower rates

- Using tax deductions on mortgage interest

👉 Over time, your investment returns can exceed your total interest paid—effectively making your loan “free”.

Best Ways To Avoid High Home Loan Interest Amount in US

Here are practical strategies:

- Choose shorter loan tenure

- Refinance when rates drop (Check Our Refinance Calculator)

- Make strategic extra payments

- Improve credit score before applying

- Compare lenders carefully

- Balance between investing & prepayment

Home Loan PITI & 401(k) Retirement Recovery Planner

This tool acts as a complete financial planner by combining:

- Mortgage planning

- Retirement strategy

- Investment optimization

It ensures you don’t sacrifice your future wealth while trying to reduce debt.

Who Should Use This Mortgage PITI & 401(k) Recovery Tool?

- First-time home buyers in the US

- Existing homeowners

- Retirement planners

- Financial advisors

- Anyone balancing debt vs investment

Conclusion

The Mortgage PITI & 401(k) Recovery Tool 2026 (US Edition) is more than just a calculator—it’s a strategic financial decision-making tool. It helps you understand the delicate balance between debt repayment and wealth creation.

Instead of blindly paying off your mortgage early, this tool empowers you to make smarter, data-driven choices that maximize your financial future.

Disclaimer: These tools are for educational and illustrative purposes only. While developed by a licensed financial professional, results are estimates and not guaranteed. Please consult with a certified advisor before making any investment or insurance decisions. Financial Guide Website is not liable for any financial loss incurred based on the use of these calculators.

It is a financial calculator that compares home loan costs (PITI) with 401(k) investment growth to optimize financial decisions.

It depends on interest rates and expected returns. If 401(k) returns are higher, investing is often better.

Yes, through compounding returns, your investments can offset or exceed your mortgage interest over time.

Principal, Interest, Taxes, and Insurance—all components of your mortgage payment.

Absolutely. It helps align mortgage decisions with long-term retirement goals.

Yes, this version is optimized for US financial systems, including 401(k), tax benefits, and mortgage structures.